![]() Accountancy

Accountancy![]()

![]() Q.1 Amit and Beena were partners in a firm sharing profits and losses in the ratio of 3 : 1. Chaman was admitted as a new partner for 1⁄6 th share in the profits. Chaman acquired 2⁄5th of his share from Amit. How much share did Chaman acquire from Beena ?

Q.1 Amit and Beena were partners in a firm sharing profits and losses in the ratio of 3 : 1. Chaman was admitted as a new partner for 1⁄6 th share in the profits. Chaman acquired 2⁄5th of his share from Amit. How much share did Chaman acquire from Beena ?

Answer: Share of profit acquired by Chaman from Aman= 1⁄6 × 2⁄5 = 2⁄30

Therefore, share of profit acquired by Chaman from Beena = 1⁄6 ⁻ 2⁄30 = 3⁄30 = 1⁄10

OR

Answer: Share of profit acquired by Chaman from Beena= 3⁄5 × 1⁄6 = 3⁄30 = 1⁄10

![]() Q. 2. Neetu, Meetu and Teetu were partners in a firm. On 1st January, 2018, Meetu retired. On Meetu’s retirement the goodwill of the firm was valued at ₹. 4,20,000. Pass necessary journal entry for the treatment of goodwill on Meetu’s retirement.

Q. 2. Neetu, Meetu and Teetu were partners in a firm. On 1st January, 2018, Meetu retired. On Meetu’s retirement the goodwill of the firm was valued at ₹. 4,20,000. Pass necessary journal entry for the treatment of goodwill on Meetu’s retirement.

Answer:

![]() Q.3. Distinguish between ‘Dissolution of partnership’ and ‘Dissolution of partnership firm’ on the basis of settlement of assets and liabilities.

Q.3. Distinguish between ‘Dissolution of partnership’ and ‘Dissolution of partnership firm’ on the basis of settlement of assets and liabilities.

Answer:

| Basic | Dissolution of partnership | Dissolution of partnership firm |

| Settlement of assetsand liabilities | Assets and liabilities are revaluedand new balance sheet is drawn | Assets are sold andliabilities are paid off |

![]() Q.4. Ritesh and Hitesh are childhood friends. Ritesh is a consultant whereas Hitesh is an architect. They contributed equal amounts and purchased a building for ₹. 2 crores. After a year, they sold it for ₹. 3 crores and shared the profits equally. Are they doing the business in partnership ? Give reason in support of your answer.

Q.4. Ritesh and Hitesh are childhood friends. Ritesh is a consultant whereas Hitesh is an architect. They contributed equal amounts and purchased a building for ₹. 2 crores. After a year, they sold it for ₹. 3 crores and shared the profits equally. Are they doing the business in partnership ? Give reason in support of your answer.

Answer: No, they are not doing business in partnership because they are not involved in doing sale and purchase of land/ plot on a regular basis/ Mere co-ownership of a property does not amount to partnership.

![]() Q.5. Is ‘Reserve Capital’ a part of ‘Unsubscribed Capital’ or ‘Uncalled Capital’ ?

Q.5. Is ‘Reserve Capital’ a part of ‘Unsubscribed Capital’ or ‘Uncalled Capital’ ?

Answer: Reserve Capital is a part of Uncalled Capital.

![]() Q.6. Give the meaning of ‘Debentures issued as Collateral Security’.

Q.6. Give the meaning of ‘Debentures issued as Collateral Security’.

Answer: When the company issues debentures to the lenders as an additonal/ secondary security, in addition to other assets already pledged/ some primary security. Such issue of debentures is called debentures issued as a collateral security.

![]() Q.7. Jayant, Kartik and Leena were partners in a firm sharing profits and losses in the ratio of 5 : 2 : 3. Kartik died and Jayant and Leena decided to continue the business. Their gaining ratio was 2 : 3.

Q.7. Jayant, Kartik and Leena were partners in a firm sharing profits and losses in the ratio of 5 : 2 : 3. Kartik died and Jayant and Leena decided to continue the business. Their gaining ratio was 2 : 3.

Calculate the new profit sharing ratio of Jayant and Leena.

Answer: Jayant’s gain= 2⁄5 × 2⁄10 = 4⁄50

Leena’s gain = 3⁄5 × 2⁄10 = 6⁄50

Jayant’s new share= 5⁄10 + 4⁄50 = 29⁄50

Leena’s new share = 3⁄10 + 6⁄50 = 21⁄50

New profit sharing ratio of Jayant and Leena = 29:21 or 29⁄50 : 21⁄50

![]() Q.8. What is meant by a ‘Share’ ? Give any two differences between ‘Preference Shares’ and ‘Equity Shares’.

Q.8. What is meant by a ‘Share’ ? Give any two differences between ‘Preference Shares’ and ‘Equity Shares’.

Answer: A Share refers to the unit into which the total share capital of the company is divided.

OR

A share means a share in the share capital of the company and includes stock.

Differences between ‘Preference Shares’ and ‘Equity Shares’:

(i) Preference Shares are shares which carry a prefrential right at the time of payment of

dividend and at the time of repayment of capital.

(ii) Equity shares are shares which do not carry a prefrential right at the time of payment of dividend and at the time of repayment of capital.

OR

Differences between ‘Preference Shares’ and ‘Equity Shares’: (Any two)

| # | Preference Shares | Equity Shares |

| (i) | Share which enjoys preferential right at the time of payment of dividend/Dividend is paid on preference sharesbefore it is paid on equity shares. | Shares which do not enjoy preferentialright at the time of payment ofdividend/Dividend is paid on equity shares after it is paid on preference shares. |

| (ii) | Enjoy preferential right at the time ofrepayment of capital. | Do not enjoy preferential right at thetime of repayment of capital. |

| (iii) | Rate of dividend may be fixed. | Rate of dividend is proposed every yearby the directors and approved by theshareholders. |

| (iv) | Preference shares may be converted into equity shares if the terms of issueprovide for it. | Equity shares are not convertible. |

| (v) | Preference shareholders have votingrights in special circumstances. | Equity shareholders have voting rightsin all circumstances. |

| (vi) | Preference shareholders do not have the right to participate in the management of the company. | Equity shareholders have the right toparticipate in the management of thecompany. |

| (vii) | Arrears on cumulative preference sharesare paid before dividend is paid onequity shares. | If dividend is not declared during theyear, it is not accumulated to be paidthe coming years. |

![]() Q.9. NK Ltd., a truck manufacturing company, is registered with an authorised capital of ₹. 1,00,00,000 divided into equity shares of ₹. 100 each. The subscribed and paid up capital of the company is ₹. 50,00,000.

Q.9. NK Ltd., a truck manufacturing company, is registered with an authorised capital of ₹. 1,00,00,000 divided into equity shares of ₹. 100 each. The subscribed and paid up capital of the company is ₹. 50,00,000.

The company decided to open technical schools in the Jhalawar district of Rajasthan to train the specially abled children of the area. It is planning to provide them employment in its various production units and industries in the neighbourhood area. To meet the capital expenditure requirements of the project, the company offered 20,000 shares to the public for subscription. The shares were fully subscribed and paid. Present the share capital in the Balance Sheet of the company as per the provisions of Schedule III of the Companies Act, 2013.

Also identify any two values that the company wants to communicate.

Answer:

Balance Sheet of NK Ltd.

As at ………………..(As per revised schedule III)

Notes to Accounts :

Values (Any two):

(i) Concern for the specially abled.

(ii) Creation of job opportunities.

(iii) Development of backward regions.

(Or any other suitable value)

![]() Q.10. Complete the following journal entries left blank in the books of VK Ltd. : VK Ltd.

Q.10. Complete the following journal entries left blank in the books of VK Ltd. : VK Ltd.

Answer:

VK Ltd.

Journal

![]() Q.11. Banwari, Girdhari and Murari are partners in a firm sharing profits and losses in the ratio of 4 : 5 : 6. On 31st March, 2014, Girdhari retired. On that date the capitals of Banwari, Girdhari and Murari before the necessary adjustments stood at ₹. 2,00,000, ₹. 1,00,000 and ₹. 50,000 respectively. On Girdhari’s retirement, goodwill of the firm was valued at ₹. 1,14,000. Revaluation of assets and reassessment of liabilities resulted in a profit of ₹. 6,000. General Reserve stood in the books of the firm at ₹. 30,000.

Q.11. Banwari, Girdhari and Murari are partners in a firm sharing profits and losses in the ratio of 4 : 5 : 6. On 31st March, 2014, Girdhari retired. On that date the capitals of Banwari, Girdhari and Murari before the necessary adjustments stood at ₹. 2,00,000, ₹. 1,00,000 and ₹. 50,000 respectively. On Girdhari’s retirement, goodwill of the firm was valued at ₹. 1,14,000. Revaluation of assets and reassessment of liabilities resulted in a profit of ₹. 6,000. General Reserve stood in the books of the firm at ₹. 30,000.

The amount payable to Girdhari was transferred to his loan account. Banwari and Murari agreed to pay Girdhari two yearly instalments of ₹. 75,000 each including interest @ 10% p.a. on the outstanding balance during the first two years and the balance including interest in the third year. The firm closes its books on 31st March every year. Prepare Girdhari’s loan account till it is finally paid showing the working notes clearly.

Answer:

Working Notes:

Calculation of amount payable to Girdhari: ₹

Girdhari’s Capital 1,00,000

Share of goodwill 38,000

Share of Revaluation profit 2,000

Share of General reserve 10,000

1,50,000

(WORKING NOTES MAY BE SHOWN IN ANY FORM)

![]() Q.12. Asha and Aditi are partners in a firm sharing profits and losses in the ratio of 3 : 2. They admit Raghav as a partner for ¼ th share in the profits of the firm. Raghav brings ₹. 6,00,000 as his capital and his share of goodwill in cash. Goodwill of the firm is to be valued at two years’ purchase of average profits of the last four years.

Q.12. Asha and Aditi are partners in a firm sharing profits and losses in the ratio of 3 : 2. They admit Raghav as a partner for ¼ th share in the profits of the firm. Raghav brings ₹. 6,00,000 as his capital and his share of goodwill in cash. Goodwill of the firm is to be valued at two years’ purchase of average profits of the last four years.

The profits of the firm during the last four years are given below :

| Year | Profit (₹) |

| 2013-14 | 3,50,000 |

| 2014-15 | 4,75,000 |

| 2015-16 | 6,70,000 |

| 2016-17 | 7,45,000 |

The following additional information is given :

(i) To cover management cost an annual charge of ₹. 56,250 should be made for the purpose of valuation of goodwill.

(ii) The closing stock for the year ended 31.3.2017 was overvalued by ₹. 15,000. Pass necessary journal entries on Raghav’s admission showing the working notes clearly.

Answer:

Working Notes:

Calculation of goodwill:

Profits

2013-14 ₹3,50,000 – ₹56,250 = ₹2,93,750

2014-15 ₹4,75,000 – ₹56,250 = ₹4,18,750

2015-16 ₹6,70,000 – ₹56,250 = ₹6,13,750

2016-17 ₹7,45,000 – ₹56,250 – ₹15,000 = ₹6,73,750

Goodwill of the firm = (₹2,93,750 + ₹4,18,750 + ₹6,13, 750 + ₹6,73,750)/4 x 2 = ₹10,00,000

Raghav’s share of goodwill = 1⁄4 x ₹10,00,000 = ₹2,50,000

OR

Answer: Calculation of goodwill:

Total Profits of four years = ₹3,50,000 + ₹4,75,000 + ₹6,70,000 + ₹7,30,000 = ₹22,25,000

Average Profits = ₹ 5,56,250 – ₹ 56,250 = ₹ 5,00,000

Goodwill of the firm = ₹ 5,00,000 x 2 = ₹10,00,000

Raghav’s share of goodwill = 1⁄4 x ₹10,00,000 = ₹2,50,000

![]() Q.13. Pranav, Karan and Rahim were partners in a firm sharing profits and losses in the ratio of 2 : 2 : 1.

Q.13. Pranav, Karan and Rahim were partners in a firm sharing profits and losses in the ratio of 2 : 2 : 1.

On 31st March, 2017 their Balance Sheet was as follows :

Balance Sheet of Pranav, Karan and Rahim as on 31.3.2017

| Liabilities | Amount ₹ | Assets | Amount ₹ |

| Creditors | 3,00,000 | Fixed Assets | 4,50,000 |

| General Reserve | 1,50,000 | Stock | 1,50,000 |

| Capitals Pranav – 2,00,000Karan – 2,00,000 Rahim – 1,00,000 |

5,00,000 |

DebtorsBank | 1,50,000 |

| Total | 9,50,000 | Total | 9,50,000 |

Karan died on 12.6.2017. According to the partnership deed, the legal representatives of the deceased partner were entitled to the following :

(i) Balance in his Capital Account.

(ii) Interest on Capital @ 12% p.a.

(iii) Share of goodwill. Goodwill of the firm on Karan’s death was valued at ₹. 60,000.

(iv) Share in the profits of the firm till the date of his death, calculated on the basis of last year’s profit. The profit of the firm for the year ended 31.3.2017 was ₹. 5,00,000.

Prepare Karan’s Capital Account to be presented to his representatives.

Answer:

Working Notes:

Interest on Capital = 12/100 x 73/365 x ₹2,00,000 = ₹4,800

Share of Profits = 2/5 x 5,00,000 x 73/365 = ₹40,000

Share of goodwill = 2/5 X ₹60,000 = ₹24,000

Share of General Reserve = 2/5 x ₹1,50,000 = ₹60,000

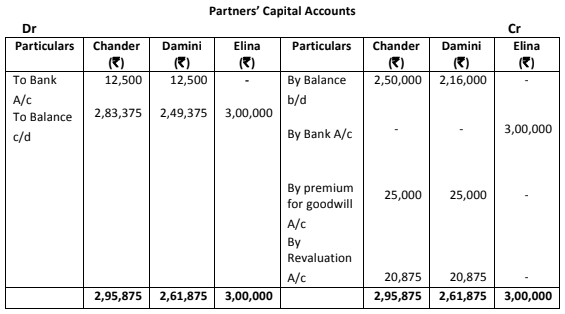

![]() Q.14. Chander and Damini were partners in a firm sharing profits and losses equally. On 31st March, 2017 their Balance Sheet was as follows :

Q.14. Chander and Damini were partners in a firm sharing profits and losses equally. On 31st March, 2017 their Balance Sheet was as follows :

On 1.4.2017, they admitted Elina as a new partner for 31 rd share in the profits on the following conditions :

(i) Elina will bring ₹. 3,00,000 as her capital and ₹. 50,000 as her share of goodwill premium, half of which will be withdrawn by Chander and Damini.

(ii) Debtors to the extent of ₹. 5,000 were unrecorded.

(iii) Furniture will be reduced by 10% and 5% provision for bad and doubtful debts will be created on bills receivables and debtors.

(iv) Value of land and building will be appreciated by 20%.

(v) There being a claim against the firm for damages, a liability to the extent of ₹. 8,000 will be created for the same.

Prepare Revaluation Account and Partners’ Capital Accounts.

Answer:

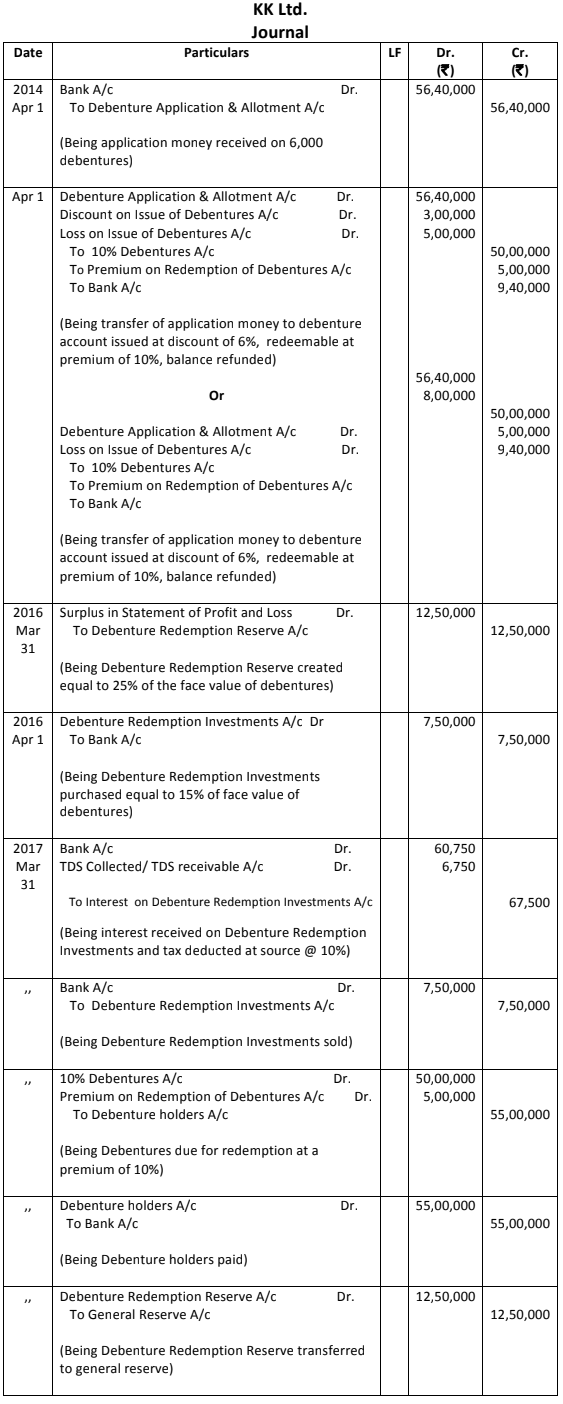

![]() Q.15. On 1st April, 2014, KK Ltd. invited applications for issuing 5,000 10% debentures of ₹. 1,000 each at a discount of 6%. These debentures were repayable at the end of 3rd year at a premium of 10%. Applications for 6,000 debentures were received and the debentures were allotted on pro-rata basis to all the applicants. Excess money received with applications was refunded.

Q.15. On 1st April, 2014, KK Ltd. invited applications for issuing 5,000 10% debentures of ₹. 1,000 each at a discount of 6%. These debentures were repayable at the end of 3rd year at a premium of 10%. Applications for 6,000 debentures were received and the debentures were allotted on pro-rata basis to all the applicants. Excess money received with applications was refunded.

The directors decided to transfer the minimum amount to Debenture Redemption Reserve on 31.3.2016. On 1.4.2016, the company invested the necessary amount in 9% bank fixed deposit as per the provisions of the Companies Act, 2013. Tax was deducted at source by bank on interest @ 10% p.a.

Pass the necessary journal entries for issue and redemption of debentures. Ignore entries relating to writing off loss on issue of ebentures and interest paid on debentures.

Answer:

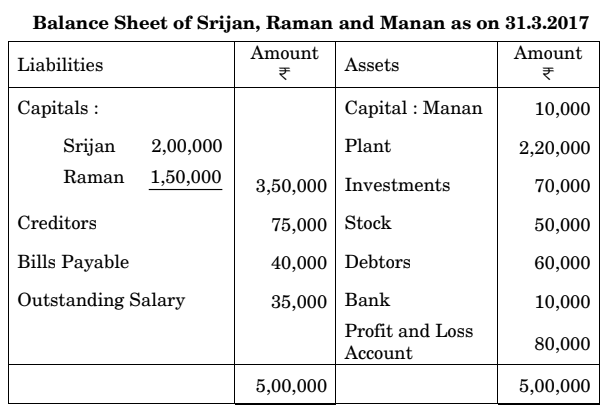

![]() Q.16. Srijan, Raman and Manan were partners in a firm sharing profits and losses in the ratio of 2 : 2 : 1. On 31st March, 2017 their Balance Sheet was as follows :

Q.16. Srijan, Raman and Manan were partners in a firm sharing profits and losses in the ratio of 2 : 2 : 1. On 31st March, 2017 their Balance Sheet was as follows :

On the above date they decided to dissolve the firm.

(i) Srijan was appointed to realise the assets and discharge the liabilities. Srijan was to receive 5% commission on sale of assets (except cash) and was to bear all expenses of realisation.

(ii) Assets were realised as follows :

Plant 85,000

Stock 33,000

Debtors 47,000

(iii) Investments were realised at 95% of the book value.

(iv) The firm had to pay ₹. 7,500 for an outstanding repair bill not provided for earlier.

(v) A contingent liability in respect of bills receivable, discounted with the bank had also materialised and had to be discharged for ₹. 15,000.

(vi) Expenses of realisation amounting to ₹. 3,000 were paid by Srijan. Prepare Realisation Account, Partners’ Capital Accounts and Bank Account.

OR

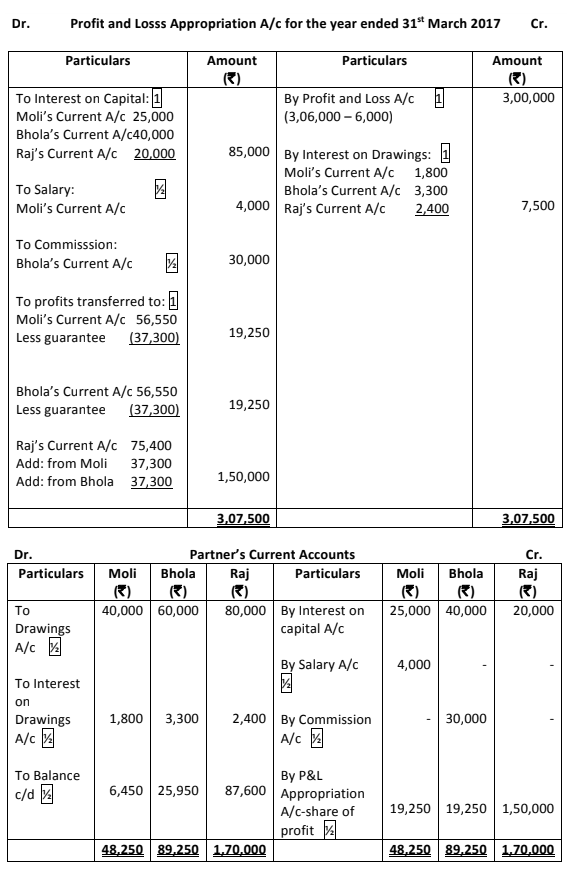

![]() Q.16. Moli, Bhola and Raj were partners in a firm sharing profits and losses in the ratio of 3 : 3 : 4. Their partnership deed provided for the following :

Q.16. Moli, Bhola and Raj were partners in a firm sharing profits and losses in the ratio of 3 : 3 : 4. Their partnership deed provided for the following :

(i) Interest on capital @ 5% p.a.

(ii) Interest on drawing @ 12% p.a.

(iii) Interest on partners’ loan @ 6% p.a.

(iv) Moli was allowed an annual salary of ₹. 4,000;

Bhola was allowed a commission of 10% of net profit as shown by Profit and Loss Account and Raj was guaranteed a profit of ₹. 1,50,000 after making all the adjustments as provided in the partnership agreement.

Their fixed capitals were Moli : ₹. 5,00,000;

Bhola : ₹. 8,00,000 and Raj : ₹. 4,00,000.

On 1st April, 2016 Bhola extended a loan of ₹. 1,00,000 to the firm. The net profit of the firm for the year ended 31st March, 2017 before interest on Bhola’s loan was ₹. 3,06,000. Prepare Profit and Loss Appropriation Account of Moli, Bhola and Raj for the year ended 31st March, 2017 and their Current Accounts assuming that Bhola withdrew ₹. 5,000 at the end of each month, Moli withdrew ₹. 10,000 at the end of each quarter and Raj withdrew ₹. 40,000 at the end of each half year.

Answer:

OR

Answer:

![]() Q.17. X Ltd. invited applications for issuing 50,000 equity shares of ₹. 10 each. The amount was payable as follows :

Q.17. X Ltd. invited applications for issuing 50,000 equity shares of ₹. 10 each. The amount was payable as follows :

On Application : ₹. 2 per share

On Allotment : ₹. 2 per share

On First Call : ₹. 3 per share

On Second and Final Call : Balance amount Applications for 70,000 shares were received. Applications for 10,000 shares were rejected and the application money was refunded. Shares were allotted to the remaining applicants on a pro-rata basis and excess money received with applications was transferred towards sums due on allotment and calls, if any. Gopal, who applied for 600 shares, paid his entire share money with application. Ghosh, who had applied for 6,000 shares, failed to pay the allotment money and his shares were immediately forfeited. These forfeited shares were re-issued to Sultan for ₹. 20,000; ₹. 4 per share paid up. The first call money and the second and final call money was called and duly received. Pass necessary journal entries for the above transactions in the books of X Ltd. Open Calls-in-Advance Account and Calls-in-Arrears Account wherever necessary.

OR

Q.17. A Ltd. invited applications for issuing 1,00,000 shares of ₹. 10 each at a premium of ₹. 1 per share. The amount was payable as follows :

On Application : ₹. 3 per share

On Allotment : ₹. 3 per share (including premium)

On First Call : ₹. 3 per share

On Second and Final Call : Balance amount

Applications for 1,60,000 shares were received.

Allotment was made on the following basis :

(i) To applicants for 90,000 shares : 40,000 shares

(ii) To applicants for 50,000 shares : 40,000 shares

(iii) To applicants for 20,000 shares : full shares

Excess money paid on application is to be adjusted against the amount due on allotment and calls.

Rishabh, a shareholder, who applied for 1,500 shares and belonged to category (ii), did not pay allotment, first and second and final call money.

Another shareholder, Sudha, who applied for 1,800 shares and belonged to category (i), did not pay the first and second and final call money.

All the shares of Rishabh and Sudha were forfeited and were subsequently re-issued at ₹. 7 per share fully paid.

Pass the necessary journal entries in the books of A Ltd. Open Calls-in-Arrears Account and Calls-in-Advance Account wherever required.

Answer

OR

Answer:

PART B

(Analysis of Financial Statements)

![]() Q.18. State the primary objective of preparing a Cash Flow Statement.

Q.18. State the primary objective of preparing a Cash Flow Statement.

Answer:The primary objective of Cash Flow Statement is to provide useful information about cash flows (inflows and outflows) of an enterprise during a particular period underoperating, investing and financing activities.

![]() Q.19.‘Interest received and paid’ is considered as which type of activity by a finance company while preparing a Cash Flow Statement ?

Q.19.‘Interest received and paid’ is considered as which type of activity by a finance company while preparing a Cash Flow Statement ?

Answer: Interest received – Operating activity.

Interest paid – Operating activity.

OR

Answer: Interest received and paid – Operating activity.

![]() Q.20. Prepare a common size Balance Sheet of KJ Ltd. from the following information :

Q.20. Prepare a common size Balance Sheet of KJ Ltd. from the following information :

Answer:

In case the examinee has prepared only columns (i) and (ii) in the correct order, one mark may be awarded.

![]() Q.21. From the following information obtained from the books of Kundan Ltd., calculate the inventory turnover ratio for the years 2015 − 16 and 2016 – 17 :

Q.21. From the following information obtained from the books of Kundan Ltd., calculate the inventory turnover ratio for the years 2015 − 16 and 2016 – 17 :

2015 − 16(₹) 2016 − 17(₹)

Inventory on 31st March 7,00,000 17,00,000

Revenue from operations 50,00,000 75,00,000

(Gross profit is 25% on cost of revenue from operations)

In the year 2015 − 16, inventory increased by ₹ 2,00,000.

Answer:

Inventory turnover ratio = Cost of Revenue from operations/Average inventory

2015-16 :

Cost of Revenue from operations= ₹50,00,000 -₹10,00,000 = ₹40,00,000

Average inventory = Opening inventory + Closing inventory /2

= (₹5,00,000 + ₹7,00,000)/2

= ₹6,00,000

Inventory turnover ratio = ₹40,00,000/₹6,00,000 = 6.67 times

2016-17 :

Cost of Revenue from operations= ₹75,00,000 – ₹15,00,000 = ₹60,00,000

Average inventory = Opening inventory + Closing inventory/2

= (₹7,00,000 + ₹17,00,000)/2

= ₹12,00,000

Inventory turnover ratio = ₹60,00,000/₹12,00,000 = 5 times

![]() Q.22. JW Ltd. was a company manufacturing geysers. As a part of its long term goal for expansion, the company decided to identify the opportunity in rural areas. Initial plan was rolled out for Bhiwani village in Haryana. Since the village did not have regular supply of electricity, the company decided to manufacture solar geysers. The core team consisting of the Regional Manager, Accountant and the Marketing Manager was taken from the Head Office and the remaining employees were selected from the village and neighbourhood areas. At the time of preparation of financial statements, the accountant of the company fell sick and the company deputed a junior accountant temporarily from the village for two months. The Balance Sheet prepared by the junior accountant showed the following items against the Major Heads and Sub-heads mentioned which were not as per Schedule III of the Companies Act, 2013.

Q.22. JW Ltd. was a company manufacturing geysers. As a part of its long term goal for expansion, the company decided to identify the opportunity in rural areas. Initial plan was rolled out for Bhiwani village in Haryana. Since the village did not have regular supply of electricity, the company decided to manufacture solar geysers. The core team consisting of the Regional Manager, Accountant and the Marketing Manager was taken from the Head Office and the remaining employees were selected from the village and neighbourhood areas. At the time of preparation of financial statements, the accountant of the company fell sick and the company deputed a junior accountant temporarily from the village for two months. The Balance Sheet prepared by the junior accountant showed the following items against the Major Heads and Sub-heads mentioned which were not as per Schedule III of the Companies Act, 2013.

| Item | Major Head/Sub-Head |

| Loose Tools | Trade Receivables |

| Cheques in Hand | Current Investments |

| Term Loan from Bank | Other Long-term Liabilities |

| Computer Software | Tangible Fixed Assets |

Identify any two values that the company wants to communicate to the society. Also present the above items under the correct major heads and sub-heads as per Schedule III of the Companies Act, 2013.

Answer:

Values (Any two):

(i) Development of rural areas.

(ii) Sensitivity towards the environment.

(iii) Generation of employment.

(Or any other suitable value)

| Item | Head | Sub-Head |

| Loose Tools | Current assets | Inventories |

| Cheques in Hand | Current assets | Cash and Cash Equivalents |

| Term Loan from Bank | Non Current Liabilities | Long Term Borrowings |

| Computer Software | Non Current Assets | Fixed – Intangible Assets |

![]() Q.23. From the following Balance Sheet of JY Ltd. as at 31st March 2017, prepare a Cash Flow Statement :

Q.23. From the following Balance Sheet of JY Ltd. as at 31st March 2017, prepare a Cash Flow Statement :

Balance Sheet of JY Ltd. as at 31.3.2017

Notes to Accounts :

Additional Information :

₹ 1,00,000, 10% debentures were issued on 31.3.2017.

Answer:

Working Notes:

Calculation of Net profit before tax:

₹

Net Profit for the year 1,25,000

Add Proposed dividend 75,000

Add Provision for tax 1,25,000

3,25,000

FULL CREDIT IS TO BE GIVEN IF AN EXAMINEE HAS TAKEN ‘SHORT TERM LOANS AND ADVANCES’ AS INCREASE IN CURRENT ASSETS UNDER OPERATING ACTIVITIES.

In that case,

CASH FROM OPERATIONS = ₹2,52,000

CASH GENERATED FROM OPERATING ACTIVITIES = ₹1,77,500

CASH USED IN INVESTING ACTIVITIES = ₹2,12,500

PART B

(Computerised Accounting)

![]() Q.18. How does the usage of computer sharpen the competitive edge and enhance the profitability of a business ?

Q.18. How does the usage of computer sharpen the competitive edge and enhance the profitability of a business ?

Answer: The quick, accurate and timely access to the information, helps decision making fast and correct, hence it helps the business to earn better.

![]() Q.19. Give an example to explain the meaning of ‘stored’ and ‘derived’ attribute.

Q.19. Give an example to explain the meaning of ‘stored’ and ‘derived’ attribute.

Answer: The information which is stored e.g. date of birth of a person is an example of stored attribute where as when his/her age is calculated automatically is derived attribute.

![]() Q.20. Name the value which represents absence of data. Also state the situations which may require the use of these values.

Q.20. Name the value which represents absence of data. Also state the situations which may require the use of these values.

Answer: The value is called “Null value” The three situations in which these can be used are

1. When a particular attribute does not apply to an entry.

2. Value of an attribute is unknown.

3. Unknown because it does not exit.

![]() Q.21. Differentiate between desktop database and server database.

Q.21. Differentiate between desktop database and server database.

Answer: (Any four)

1. Application : Desktop database can be used by a single user server data base can

be used by many users at the same time.

2. Additional provision for reliability : Desktop database

Doesn’t present this but these provisions are available in server based database.

3. Cost : Desktop database tend to cost less than the server database.

4. Flexibility regarding the performance in front end applications : It is not present in desktop database but server database provide this flexibility.

5. Suitability : Desktop database are suitable for small/home offices and server

database are more suitable for large business organisations.

Q.22. Give four limitations of computerised accounting system.

Answer: Following are the limitations of computerised accounting softwares :

1. Faster obsolescence of technology necessitates investment in shorter period of time.

2. Data may be lost or corrupted due to power interruptions.

3. Data are prone to hacking.

4. Un-programmed and un-specified reports cannot be granted .

![]() Q.23. ABC Ltd. operates in two cities Bengaluru and Mangaluru. House Rent Allowance for Bengaluru is ₹ 5,000 and for Mangaluru is ₹ 4,000. Dearness Allowance is calculated on Basic Pay as follows :

Q.23. ABC Ltd. operates in two cities Bengaluru and Mangaluru. House Rent Allowance for Bengaluru is ₹ 5,000 and for Mangaluru is ₹ 4,000. Dearness Allowance is calculated on Basic Pay as follows :

15% of Basic Pay if basic pay is less than ₹ 15,000.

10% of Basic Pay if basic pay is greater than ₹ 15,000.

Standard number of days are taken as 30 days in a month.

Calculate the amount using Excel :

(i) Gross Salary of Mr. Mahesh, who is working in Bengaluru. He has availed leave without pay for 3 days and his Basic Pay is ₹ 25,000.

(ii) Gross Salary of Mr. Ranjan, who is working in Mangaluru. Basic Pay of Mr. Ranjan is ₹ 14,000.

Answer:

Gross salary of Mr. Mahesh and Ranjan

Basic pay of Mahesh Column A1 = 25000

Basic pay of Ranjan column A2 = 14000

Basic pay earned for Mahesh column B1 = A1* 27/30 = 22500

Basic pay earned for Ranjan column B2 = A2 = 14000

HRA for Mahesh Column C1 = 5000

HRA for Ranjan Column C2 = 4000

DA for Mahesh Column D1 = IF (A1>15000, 10/100*B1, 15/100*B1)

DA for Ranjan Column D2 = IF (A2 > 15000, 10/100*B2, 5/100*B2)

D1 = 2250

D2 = 2100

Gross salary for Mahesh = Column E1 = SUM (B1,C1,D1)

Gross salary for Ranjan = Column E2 = SUM (B2,C2,D2)

Mr. Mahesh’s Salary E1 = 22500 + 5000 + 2250 = ₹29750

Mr. Ranjan’s Salary E2 = 14000 + 4000 + 2100 = ₹20100