![]() Accountancy

Accountancy![]()

![]() Q.1. Distinguish between ‘Fixed Capital Account’ and ‘Fluctuating Capital Account’ on the basis of credit balance.

Q.1. Distinguish between ‘Fixed Capital Account’ and ‘Fluctuating Capital Account’ on the basis of credit balance.

Answer: Fixed Capital Accounts always show a credit balance while fluctuating capital accounts may show credit or debit balance.

![]() Q.2. A and B were partners in a firm sharing profits and losses in the ratio of 5 : 3. They admitted C as a new partner. The new profit sharing ratio between A, B and C was 3 : 2 : 3. A surrendered ⅕th of his share in favour of C. Calculate B’s sacrifice.

Q.2. A and B were partners in a firm sharing profits and losses in the ratio of 5 : 3. They admitted C as a new partner. The new profit sharing ratio between A, B and C was 3 : 2 : 3. A surrendered ⅕th of his share in favour of C. Calculate B’s sacrifice.

Answer: A’s Old Share = 5/8

A’s Sacrifice = 1/5 of 5/8 = 1/8

C’s Share = 3/8

B’s Sacrifice = C’s share – A’s sacrifice = 3/8 – 1/8 = 2/8

OR

Answer: B’s Old Share = 3/8

B’s new share = 2/8

B’s Sacrifice = 3/8 – 2/8 = 1/8

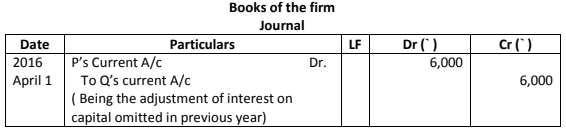

![]() Q.3. P and Q were partners in a firm sharing profits and losses equally. Their fixed capitals were ₹ 2,00,000 and ₹ 3,00,000 respectively. The partnership deed provided for interest on capital @ 12% per annum. For the year ended 31st March, 2016, the profits of the firm were distributed without providing interest on capital. Pass necessary adjustment entry to rectify the error.

Q.3. P and Q were partners in a firm sharing profits and losses equally. Their fixed capitals were ₹ 2,00,000 and ₹ 3,00,000 respectively. The partnership deed provided for interest on capital @ 12% per annum. For the year ended 31st March, 2016, the profits of the firm were distributed without providing interest on capital. Pass necessary adjustment entry to rectify the error.

Answer:

![]() Q.4. X Ltd. invited applications for issuing 500, 12% debentures of ₹ 100 each at a discount of 5%. These debentures were redeemable after three years at par. Applications for 600 debentures were received. Pro-rata allotment was made to all the applicants.

Q.4. X Ltd. invited applications for issuing 500, 12% debentures of ₹ 100 each at a discount of 5%. These debentures were redeemable after three years at par. Applications for 600 debentures were received. Pro-rata allotment was made to all the applicants.

Pass necessary journal entries for the issue of debentures assuming that the whole amount was payable with the application.

Answer:

![]() Q.5. Z Ltd. forfeited 1,000 equity shares of ₹ 10 each for the non-payment of the first call of ₹ 2 per share. The final call of ₹ 3 per share was yet to be made. Calculate the maximum amount of discount at which these shares can be reissued.

Q.5. Z Ltd. forfeited 1,000 equity shares of ₹ 10 each for the non-payment of the first call of ₹ 2 per share. The final call of ₹ 3 per share was yet to be made. Calculate the maximum amount of discount at which these shares can be reissued.

Answer: The maximum amount of discount at which these shares can be re-issued is ₹5 per share or ₹ 5000.

![]() Q.6. Durga and Naresh were partners in a firm. They wanted to admit five more members to the firm. List any two categories of individuals other than minors who cannot be admitted by them.

Q.6. Durga and Naresh were partners in a firm. They wanted to admit five more members to the firm. List any two categories of individuals other than minors who cannot be admitted by them.

Answer: Any two of the following:

• Persons of unsound mind / Lunatics

• Insolvent persons

• Any other individual who has been disqualified by law

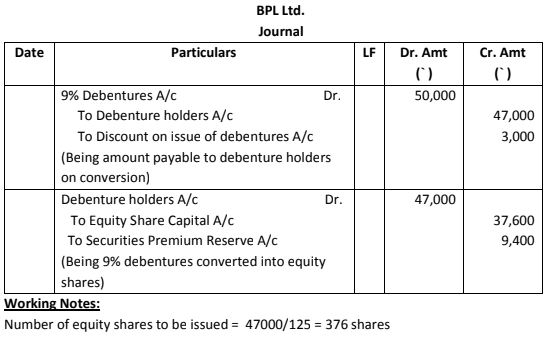

![]() Q.7. BPL Ltd. converted 500, 9% debentures of ₹ 100 each issued at a discount of 6% into equity shares of ₹ 100 each issued at a premium of ₹ 25 per share. Discount on issue of 9% debentures has not yet been written off.

Q.7. BPL Ltd. converted 500, 9% debentures of ₹ 100 each issued at a discount of 6% into equity shares of ₹ 100 each issued at a premium of ₹ 25 per share. Discount on issue of 9% debentures has not yet been written off.

Showing your working notes clearly, pass necessary journal entries for conversion of 9% debentures into equity shares.

Answer:

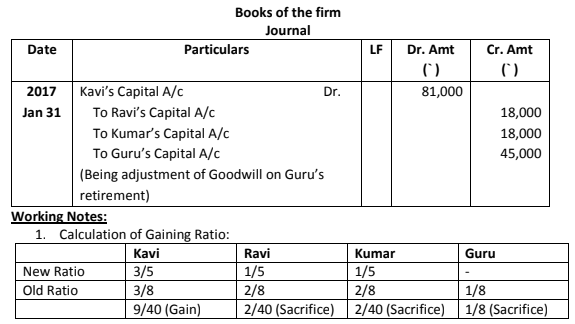

![]() Q.8. Kavi, Ravi, Kumar, and Guru were partners in a firm sharing profits in the ratio of 3: 2: 2: 1. On 1.2.2017, Guru retired and the new profit sharing ratio decided between Kavi, Ravi and Kumar were 3 : 1: 1. On Guru’s retirement, the goodwill of the firm was valued at ₹ 3,60,000.

Q.8. Kavi, Ravi, Kumar, and Guru were partners in a firm sharing profits in the ratio of 3: 2: 2: 1. On 1.2.2017, Guru retired and the new profit sharing ratio decided between Kavi, Ravi and Kumar were 3 : 1: 1. On Guru’s retirement, the goodwill of the firm was valued at ₹ 3,60,000.

Showing your working notes clearly, pass necessary journal entry in the books of the firm for the treatment of goodwill on Guru’s retirement.

Answer:

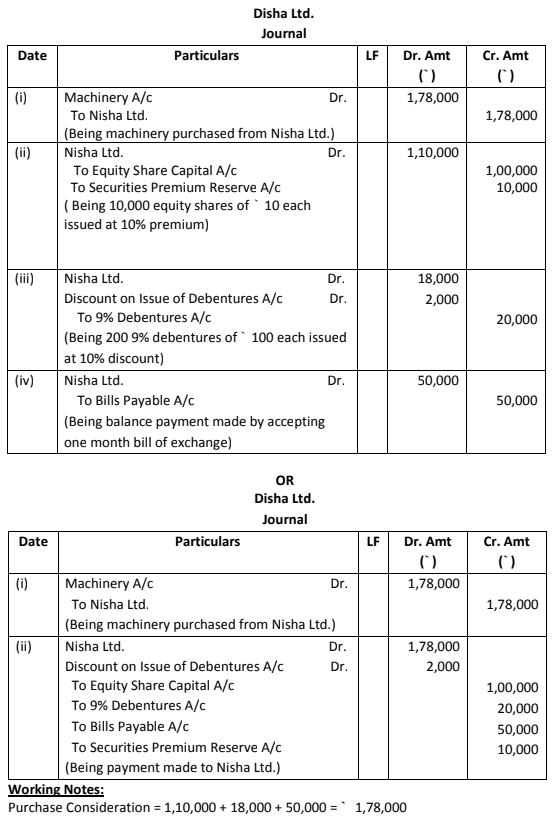

![]() Q.9. Disha Ltd. purchased machinery from Nisha Ltd. and paid to Nisha Ltd. as follows :

Q.9. Disha Ltd. purchased machinery from Nisha Ltd. and paid to Nisha Ltd. as follows :

(i) By issuing 10,000, equity shares of ₹ 10 each at a premium of 10%.

(ii) By issuing 200, 9% debentures of ₹ 100 each at a discount of 10%.

(iii) Balance by accepting a bill of exchange of ₹ 50,000 payable after one month.

Pass necessary journal entries in the books of Disha Ltd. for the purchase of machinery and making payment to Nisha Ltd.

Answer:

![]() Q.10. Ganesh Ltd. is registered with an authorized capital of ₹ 10,00,00,000 divided into equity shares of ₹ 10 each. Subscribed and fully paid-up capital of the company was ₹ 6,00,00,000. For providing employment to the local youth and for the development of the tribal areas of Arunachal Pradesh the company decided to set up a hydropower plant there. The company also decided to open skill development centers in Itanagar, Pasighat, and Tawang. To meet its new financial requirements, the company decided to issue 1,00,000 equity shares of ₹ 10 each and 1,00,000, 9% debentures of ₹ 100 each. The debentures were redeemable after five years at par. The issue of shares and debentures was fully subscribed. A shareholder holding 2,000 shares failed to pay the final call of ₹ 2 per share. Show the share capital in the Balance Sheet of the company as per the provisions of Schedule III of the Companies Act, 2013. Also, identify any two values that the company wishes to propagate.

Q.10. Ganesh Ltd. is registered with an authorized capital of ₹ 10,00,00,000 divided into equity shares of ₹ 10 each. Subscribed and fully paid-up capital of the company was ₹ 6,00,00,000. For providing employment to the local youth and for the development of the tribal areas of Arunachal Pradesh the company decided to set up a hydropower plant there. The company also decided to open skill development centers in Itanagar, Pasighat, and Tawang. To meet its new financial requirements, the company decided to issue 1,00,000 equity shares of ₹ 10 each and 1,00,000, 9% debentures of ₹ 100 each. The debentures were redeemable after five years at par. The issue of shares and debentures was fully subscribed. A shareholder holding 2,000 shares failed to pay the final call of ₹ 2 per share. Show the share capital in the Balance Sheet of the company as per the provisions of Schedule III of the Companies Act, 2013. Also, identify any two values that the company wishes to propagate.

Answer:

Values (Any two):

• Providing employment opportunities to the local youth.

• Promotion of development in tribal areas.

• Promotion of skill development in Arunachal Pradesh.

• Paying attention to regions of social unrest.

(Or any other suitable value)

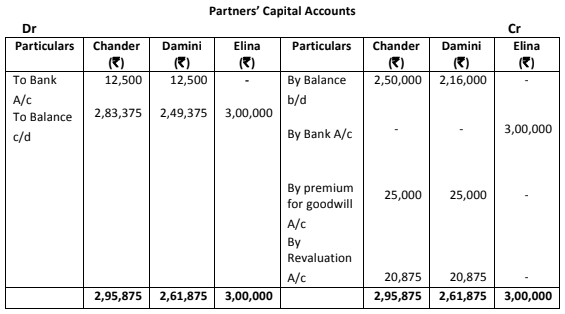

![]() Q.11. Madhu and Neha were partners in the firm sharing profits and losses in the ratio of 3: 5. Their fixed capitals were ₹ 4,00,000 and ₹ 6,00,000 respectively. On 1.1.2016, Tina was admitted as a new partner for 41 to share in the profits. Tina acquired her share of profit from Neha. Tina brought ₹ 4,00,000 as her capital which was to be kept fixed like the capitals of Madhu and Neha. Calculate the goodwill of the firm on Tina’s admission and the new profit sharing ratio of Madhu, Neha, and Tina. Also, pass necessary journal entry for the treatment of goodwill on Tina’s admission considering that Tina did not bring her share of goodwill premium in cash.

Q.11. Madhu and Neha were partners in the firm sharing profits and losses in the ratio of 3: 5. Their fixed capitals were ₹ 4,00,000 and ₹ 6,00,000 respectively. On 1.1.2016, Tina was admitted as a new partner for 41 to share in the profits. Tina acquired her share of profit from Neha. Tina brought ₹ 4,00,000 as her capital which was to be kept fixed like the capitals of Madhu and Neha. Calculate the goodwill of the firm on Tina’s admission and the new profit sharing ratio of Madhu, Neha, and Tina. Also, pass necessary journal entry for the treatment of goodwill on Tina’s admission considering that Tina did not bring her share of goodwill premium in cash.

Answer:

(a) Calculation of Hidden Goodwill:

Tina’s share = 1⁄4

Tina’s Capital = ₹ 4,00,000

(a) Total capital of the new firm = 4,00,000 × 4 = 16,00,000

(b) Existing total capital of Madhu, Neha and Tina

= ₹ 4,00,000 + ₹ 6,00 000 + ₹ 4,00,000

= ₹ 14,00,000 Goodwill of the firm

= 16,00,000-14,00,000 = 2,00,000

Thus, Tina’s share of goodwill = 1⁄4 × 2,00,000 = 50,000

(b) Calculation of New Profit Sharing ratio : Madhu’s new share

= 3/8 Neha’s new share = 5/8 – 1/4

= 3/8 Tina’s share = 1⁄4

i.e. 2/8 New Ratio = 3:3:2

(c)

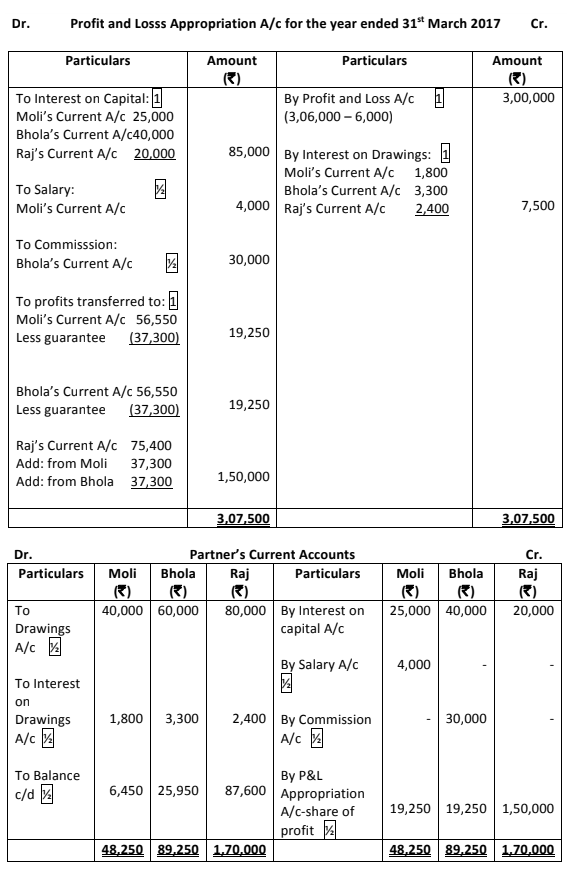

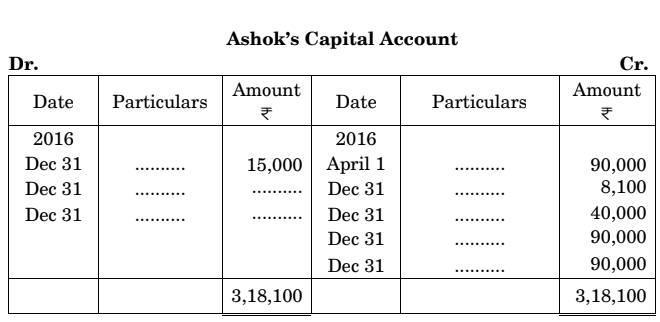

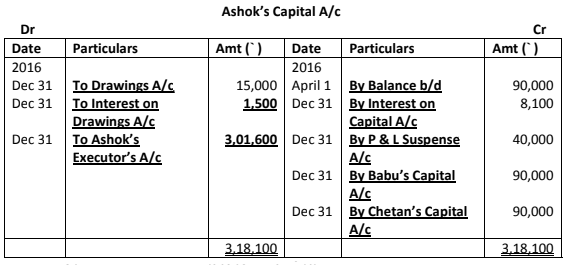

![]() Q.12. Ashok, Babu, and Chetan were partners in firm sharing profits in the ratio of 4 : 3 : 3. The firm closes its books on 31st March every year. On 31st December 2016, Ashok died. The partnership deed provided that on the death of a partner his executors will be entitled to the following :

Q.12. Ashok, Babu, and Chetan were partners in firm sharing profits in the ratio of 4 : 3 : 3. The firm closes its books on 31st March every year. On 31st December 2016, Ashok died. The partnership deed provided that on the death of a partner his executors will be entitled to the following :

(i) Balance in his capital account. On 1.4.2016, there was a balance of ₹ 90,000 in Ashok’s Capital Account.

(ii) Interest on capital @ 12% per annum.

(iii) His share in the profits of the firm in the year of his death will be calculated on the basis of the rate of net profit on sales of the previous year, which was 25%. The sales of the firm till 31st December 2016 were ₹ 4,00,000.

(iv) His share in the goodwill of the firm. The goodwill of the firm on Ashok’s death was valued at ₹ 4,50,000.

The partnership deed also provided for the following deductions from the amount payable to the executor of the deceased partner :

(i) His drawings in the year of his death. Ashok’s drawings till 31.12.2016 were ₹ 15,000.

(ii) Interest on drawings @ 12% per annum which was calculated as

₹ 1,500. The accountant of the firm prepared Ashok’s Capital Account to be presented to the executor of Ashok but in a hurry he left it incomplete. Ashok’s Capital Account as prepared by the firm’s accountant is given below :

You are required to complete Ashok’s Capital Account.

Answer:

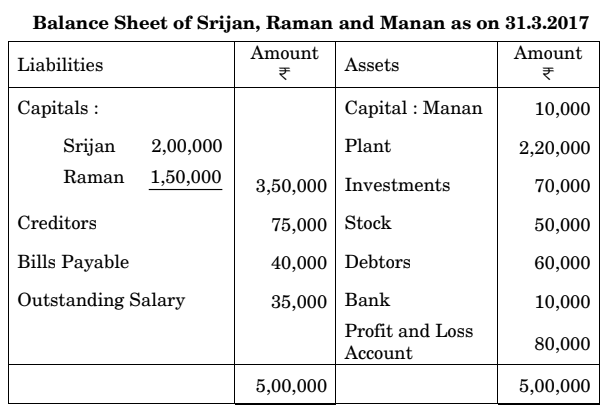

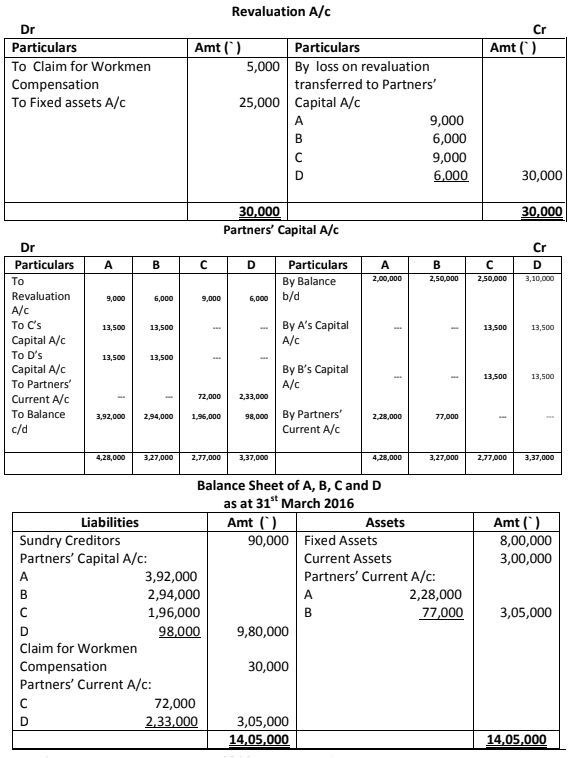

![]() Q.13. A, B, C, and D were partners in a firm sharing profits in the ratio of 3: 2 : 3: 2. On 1.4.2016, their Balance Sheet was as follows :

Q.13. A, B, C, and D were partners in a firm sharing profits in the ratio of 3: 2 : 3: 2. On 1.4.2016, their Balance Sheet was as follows :

From the above date, the partners decided to share the future profits in the ratio of 4 : 3: 2: 1. For this purpose, the goodwill of the firm was valued at ₹ 2,70,000. It was also considered that :

(i) The claim against Workmen Compensation Reserve has been estimated at ₹30,000 and fixed assets will be depreciated by ₹ 25,000.

(ii) Adjust the capitals of the partners according to the new profit sharing ratio by opening the Current Accounts of the partners.

Prepare Revaluation Account, Partners’ Capital Account, and the Balance Sheet of the reconstituted firm.

Answer:

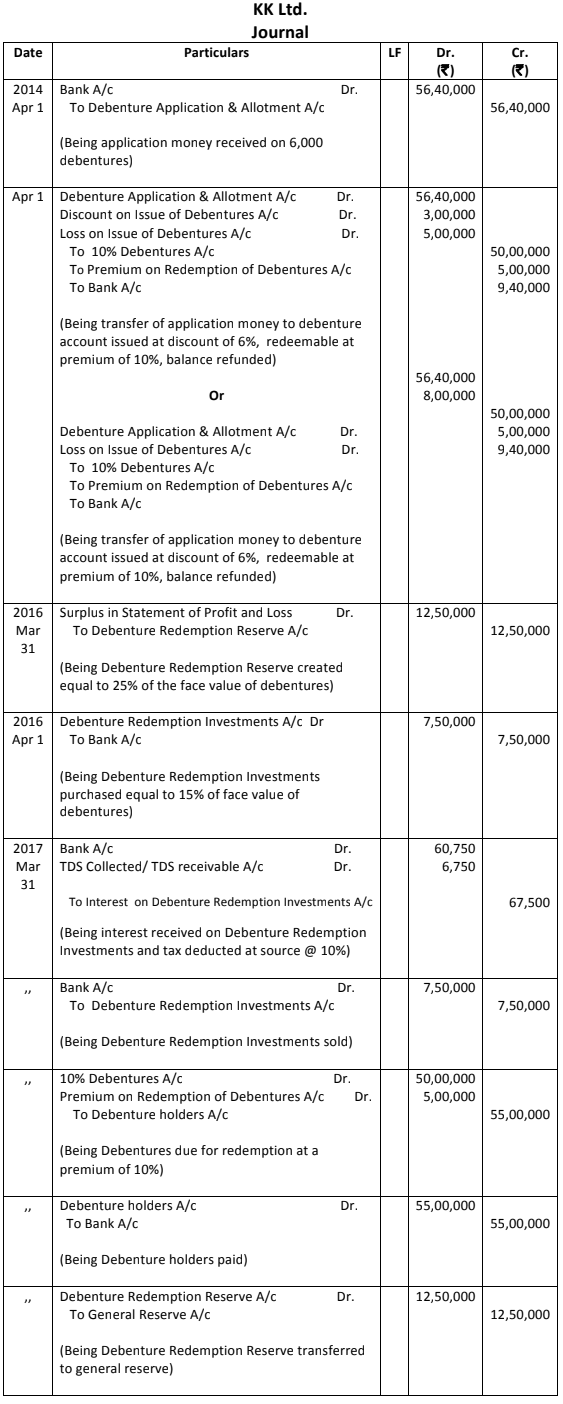

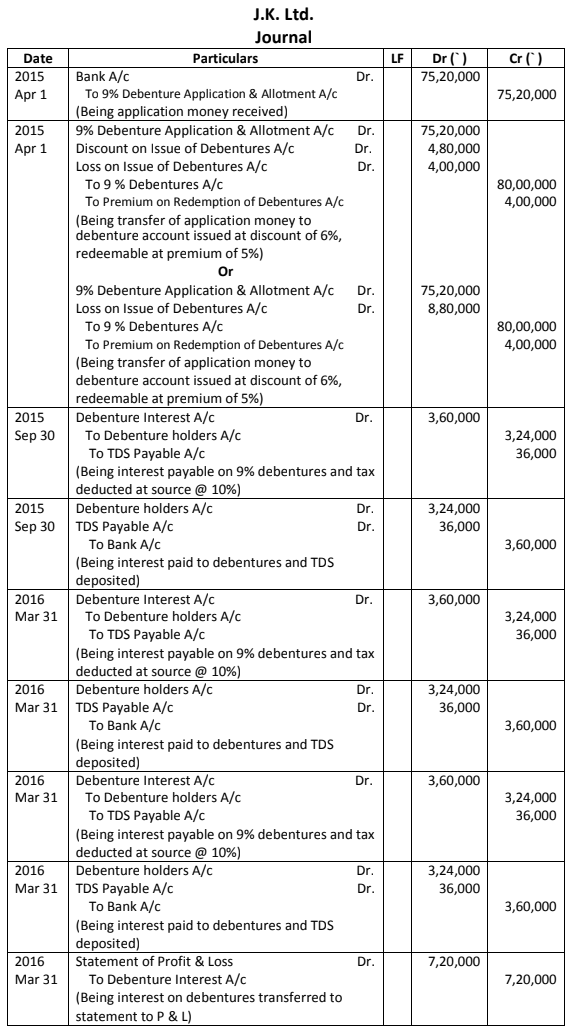

![]() Q.14. On 1.4.2015, J.K. Ltd. issued 8,000, 9% debentures of ₹ 1,000 each at a discount of 6%, redeemable at a premium of 5% after three years. The company closes its books on 31st March every year. Interest on 9% debentures is payable on 30th September and 31st March every year. The rate of tax deducted at the source is 10%.

Q.14. On 1.4.2015, J.K. Ltd. issued 8,000, 9% debentures of ₹ 1,000 each at a discount of 6%, redeemable at a premium of 5% after three years. The company closes its books on 31st March every year. Interest on 9% debentures is payable on 30th September and 31st March every year. The rate of tax deducted at the source is 10%.

Pass necessary journal entries for the issue of debentures and debenture interest for the year ended 31.3.2016.

Answer:

![]() Q.15. Pass necessary journal entries on the dissolution of a partnership firm in the following cases :

Q.15. Pass necessary journal entries on the dissolution of a partnership firm in the following cases :

(i) Dissolution expenses were ₹ 800.

(ii) Dissolution expenses ₹ 800 were paid by Prabhu, a partner.

(iii) Geeta, a partner, was appointed to look after the dissolution work, for which she was allowed a remuneration of ₹ 10,000. Geeta agreed to bear the dissolution expenses. Actual dissolution expenses of ₹ 9,500 were paid by Geeta.

(iv) Janki, a partner, agreed to look after the dissolution work for a commission of ₹ 5,000. Janki agreed to bear the dissolution expenses. Actual dissolution expenses of ₹ 5,500 were paid by Mohan, another partner, on behalf of Janki.

(v) A partner, Kavita, agreed to look after the dissolution process for a commission of ₹ 9,000. She also agreed to bear the dissolution expenses. Kavita took over the furniture of ₹ 9,000 for her commission. Furniture had already been transferred to realisation account.

(vi) A debtor, Ravinder, for ₹ 19,000 agreed to pay the dissolution expenses which were ₹ 18,000 in full settlement of his debt.

Answer:

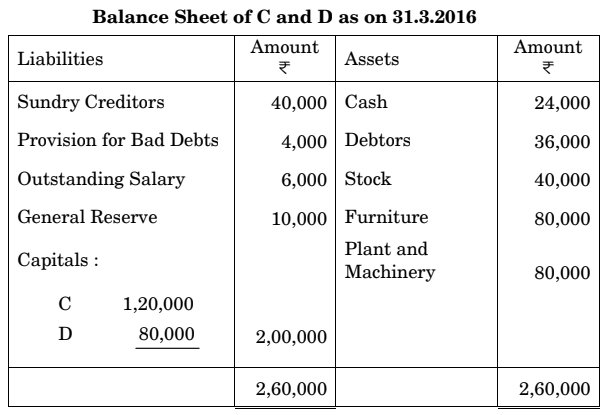

![]() Q.16. C and D are partners in a firm sharing profits in the ratio of 4: 1. On 31.3.2016, their Balance Sheet was as follows :

Q.16. C and D are partners in a firm sharing profits in the ratio of 4: 1. On 31.3.2016, their Balance Sheet was as follows :

On the above date, E was admitted for 1⁄4th share in the profits on the following terms :

(i) E will bring ₹ 1,00,000 as his capital and ₹ 20,000 for his share of goodwill premium, half of which will be withdrawn by C and D.

(ii) Debtors ₹ 2,000 will be written off as bad debts and a provision of 4% will be created on debtors for bad and doubtful debts.

(iii) Stock will be reduced by ₹ 2,000, furniture will be depreciated by ₹ 4,000 and 10% depreciation will be charged on plant and machinery.

(iv) Investments of ₹ 7,000 not shown in the Balance Sheet will be taken into account.

(v) There was an outstanding repairs bill of ₹ 2,300 which will be recorded in the books.

Pass necessary journal entries for the above transactions in the books of the firm on E’s admission.

OR

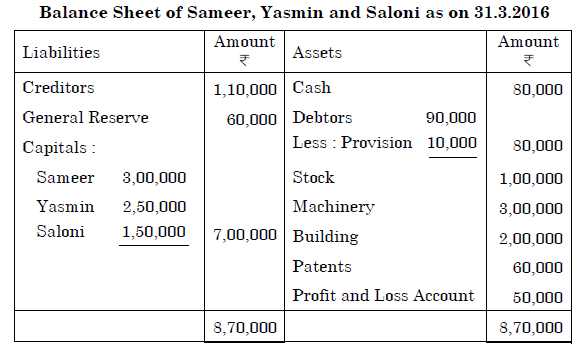

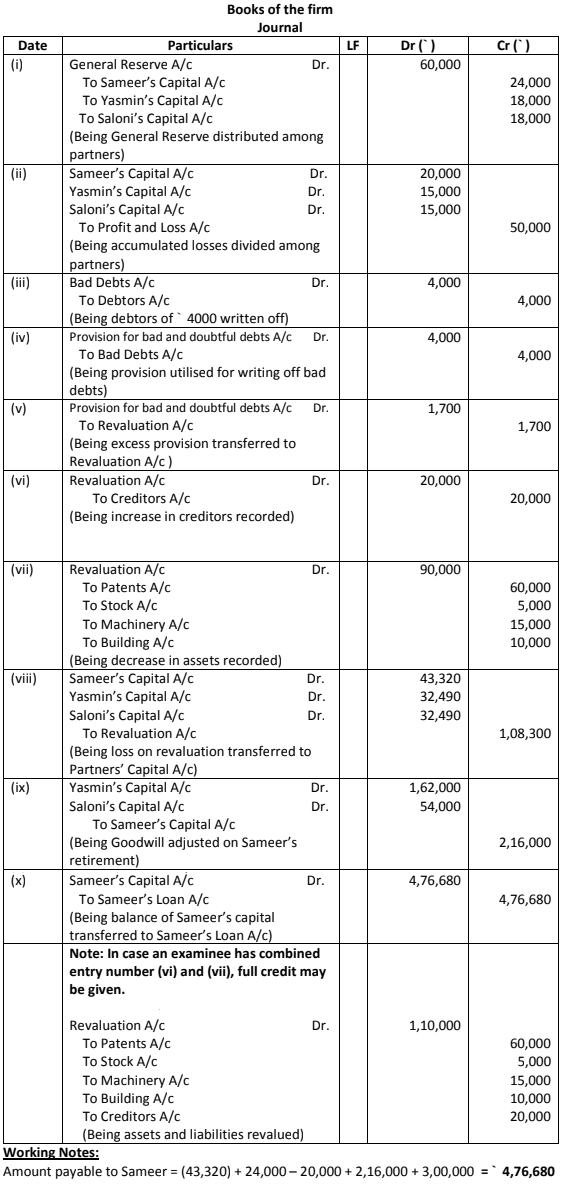

![]() Q.16. Sameer, Yasmin, and Saloni were partners in the firm sharing profits and losses in the ratio of 4 : 3 : 3. On 31.3.2016, their Balance Sheet was as follows :

Q.16. Sameer, Yasmin, and Saloni were partners in the firm sharing profits and losses in the ratio of 4 : 3 : 3. On 31.3.2016, their Balance Sheet was as follows :

On the above date, Sameer retired and it was agreed that :

(i) Debtors of ₹ 4,000 will be written off as bad debts and a provision of 5% on debtors for bad and doubtful debts will be maintained.

(ii) An unrecorded creditor of ₹ 20,000 will be recorded.

(iii) Patents will be completely written off and 5% depreciation will be charged on stock, machinery and building.

(iv) Yasmin and Saloni will share future profits in the ratio of 3: 2.

(v) Goodwill of the firm on Sameer’s retirement was valued at ₹ 5,40,000.

Pass necessary journal entries for the above transactions in the books of the firm on Sameer’s retirement.

Answer:

OR

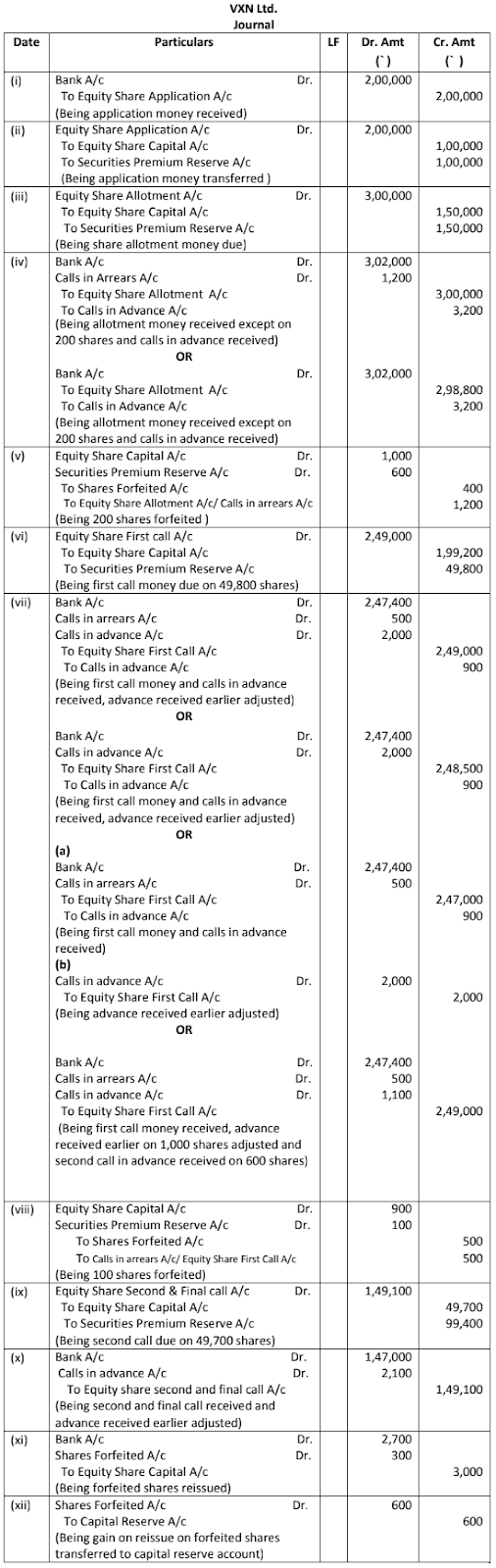

![]() Q.17. VXN Ltd. invited applications for issuing 50,000 equity shares of ₹ 10 each at a premium of ₹ 8 per share. The amount was payable as follows :

Q.17. VXN Ltd. invited applications for issuing 50,000 equity shares of ₹ 10 each at a premium of ₹ 8 per share. The amount was payable as follows :

On Application: ₹ 4 per share (including ₹ 2 premium)

On Allotment: ₹ 6 per share (including ₹ 3 premium)

On First Call: ₹ 5 per share (including ₹ 1 premium)

On Second and Final Call: Balance Amount

The issue was fully subscribed. Gopal, a shareholder holding 200 shares, did not pay the allotment money and Madhav, a holder of 400 shares, paid his entire share money along with the allotment money. Gopal’s shares were immediately forfeited after allotment. Afterward, the first call was made. Krishna, a holder of 100 shares, failed to pay the first call money and Girdhar, a holder of 300 shares, paid the second call money also along with the first call. Krishna’s shares were forfeited immediately after the first call. The second and final call was made afterward and was duly received. All the forfeited shares were reissued at ₹ 9 per share fully paid up.

Pass necessary journal entries for the above transactions in the books of the company.

OR

![]() Q.17. JJK Ltd. invited applications for issuing 50,000 equity shares of ₹ 10 each at par. The amount was payable as follows :

Q.17. JJK Ltd. invited applications for issuing 50,000 equity shares of ₹ 10 each at par. The amount was payable as follows :

On Application: ₹ 2 per share

On Allotment: ₹ 4 per share

On First and Final Call: Balance Amount

The issue was oversubscribed three times. Applications for 30% shares were rejected and money refunded. The allotment was made to the remaining applicants as follows :

Category No. of Shares Applied No. of Shares Allotted

I 80,000 40,000

II 25,000 10,000

Excess money paid by the applicants who were allotted shares was adjusted towards the sums due on allotment.

Deepak, a shareholder belonging to Category I, who had applied for 1,000 shares, failed to pay the allotment money. Raju, a shareholder holding 100 shares, also failed to pay the allotment money. Raju belonged to Category II. Shares of both Deepak and Raju were forfeited immediately after allotment. Afterward, the first and final call was made and was duly received. The forfeited shares of Deepak and Raju were reissued at ₹ 11 per share fully paid up.

Pass necessary journal entries for the above transactions in the books of the company.

Answer:

OR

Answer:

PART B

(Analysis of Financial Statements)

![]() Q.18. Normally, what should be the maturity period for a short-term investment from the date of its acquisition to be qualified as cash equivalents?

Q.18. Normally, what should be the maturity period for a short-term investment from the date of its acquisition to be qualified as cash equivalents?

Answer: Maximum maturity period is 90 days/ 3 months for a short-term investment from the date of acquisition to be qualified as cash equivalents.

![]() Q.19. State the primary objective of preparing a cash flow statement.

Q.19. State the primary objective of preparing a cash flow statement.

Answer: To find out the inflows and outflows of cash and cash equivalents from Operating, Investing, and Financing activities.

![]() Q.20. What is meant by ‘Analysis of Financial Statements’? State any two objectives of such an analysis.

Q.20. What is meant by ‘Analysis of Financial Statements’? State any two objectives of such an analysis.

Answer: Analysis of Financial Statements is the process of critical evaluation of the financial information contained in the financial statements in order to understand and make decisions regarding the operations of the firm.

(Or any other suitable meaning)

Objectives of ‘Financial Statements Analysis’: (Any two)

(i) Assessing the earning capacity or profitability of the firm as a whole as well as its different departments so as to judge the financial health of the firm.

(ii) Assessing managerial efficiency by using financial ratios to identify favorable and unfavorable variations in managerial performance.

(iii) Assessing the short-term and the long-term solvency of the enterprise to assess the ability of the company to repay principal amount and interest.

(iv) Assessing the performance of the business in comparison to that of others through inter-firm comparison.

(v) Assessing developments in the future by forecasting and preparing budgets.

(vi) To Ascertain the relative importance of different components of the financial position of the firm.

![]() Q.21. The proprietary ratio of M. Ltd. is 0·80: 1. State with reasons whether the following transactions will increase, decrease, or not change the proprietary ratio :

Q.21. The proprietary ratio of M. Ltd. is 0·80: 1. State with reasons whether the following transactions will increase, decrease, or not change the proprietary ratio :

(i) Obtained a loan from bank ₹ 2,00,000 payable after five years.

(ii) Purchased machinery for cash ₹ 75,000.

(iii) Redeemed 5% redeemable preference shares ₹ 1,00,000.

(iv) Issued equity shares to the vendors of machinery purchased for ₹ 4,00,000.

Answer:

| Transaction | Effect on Quick Ratio | Reasons |

| (i) | Decrease | No change in Shareholders’ funds but total assets will increase by ₹ 2,00,000 |

| (ii) | No Change | No change in total assets and Shareholders’ funds |

| (iii) | Decrease | Both Shareholders’ funds and total assets are decreased by same amount |

| (iv) | Increase | Shareholders’ funds and total assets both are increased |

![]() Q.22. Financial statements are prepared following the consistent accounting concepts, principles, procedures, and also the legal environment in which the business organizations operate. These statements are the sources of information on the basis of which conclusions are drawn about the profitability and financial position of a company so that their users can easily understand and use them in their economic decisions in a meaningful way. From the above statement identify any two values that a company should observe while preparing its financial statements. Also, state under which major headings and sub-headings the following items will be presented in the Balance Sheet of a company as per Schedule III of the Companies Act, 2013.

Q.22. Financial statements are prepared following the consistent accounting concepts, principles, procedures, and also the legal environment in which the business organizations operate. These statements are the sources of information on the basis of which conclusions are drawn about the profitability and financial position of a company so that their users can easily understand and use them in their economic decisions in a meaningful way. From the above statement identify any two values that a company should observe while preparing its financial statements. Also, state under which major headings and sub-headings the following items will be presented in the Balance Sheet of a company as per Schedule III of the Companies Act, 2013.

(i) Capital Reserve

(ii) Calls-in-Advance

(iii) Loose Tools

(iv) Bank Overdraft

Answer:

Values (Any two):

• Transparency

• Consistency

• Following rules and regulations / Ethical code of conduct

• Honesty and loyalty towards owners

• Providing authentic information to users

(Or any other suitable value)

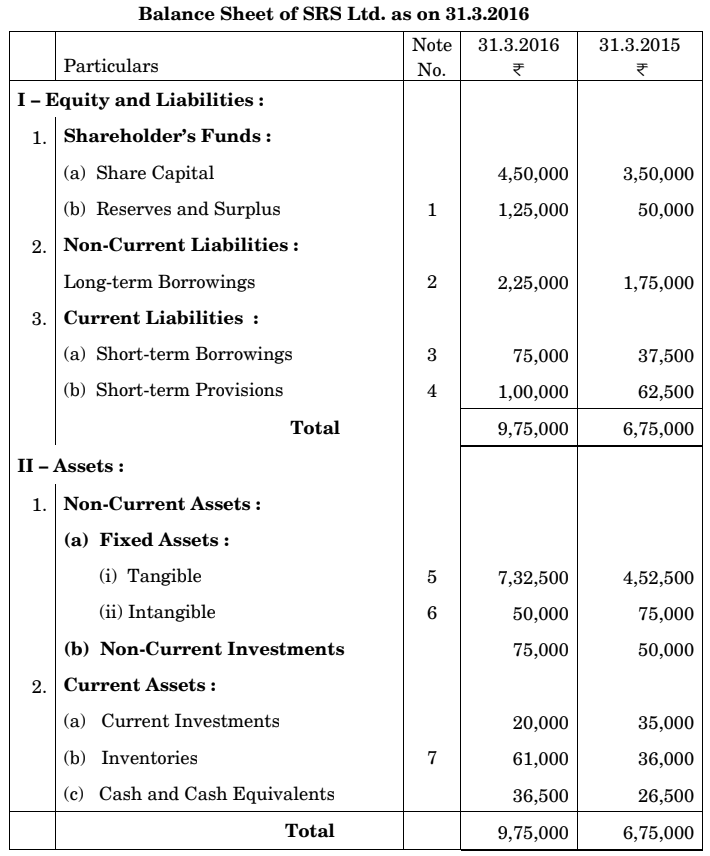

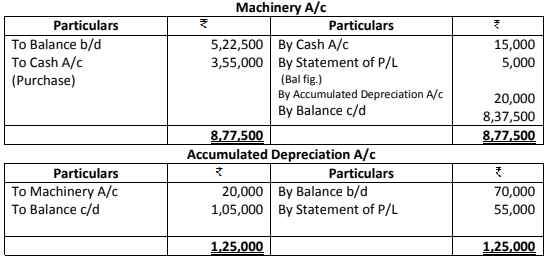

![]() Q.23. From the following Balance Sheet of SRS Ltd. and the additional information as of 31.3.2016, prepare a Cash Flow Statement :

Q.23. From the following Balance Sheet of SRS Ltd. and the additional information as of 31.3.2016, prepare a Cash Flow Statement :

Notes to Accounts

Additional Information :

(i) ₹ 50,000, 12% debentures were issued on 31.3.2016.

(ii) During the year a piece of machinery costing ₹ 40,000, on which accumulated depreciation was ₹ 20,000, was sold at a loss of ₹ 5,000.

Answer:

Notes:

Calculation of Net Profit before tax:

Net profit as per statement of Profit & Loss 75,000

Add: Proposed Dividend 1,00,000

Net Profit before tax & extraordinary items 1,75,000

PART B

(Computerized Accounting)

![]() Q.18. What is meant by a ‘Database Report’ ?

Q.18. What is meant by a ‘Database Report’ ?

Answer: A database report is the formatted result of database queries and contains useful data for decision-making and analysis.

![]() Q.19. What is meant by a ‘Query’ ?

Q.19. What is meant by a ‘Query’ ?

Answer: Queries provide the capability of combined data from multiple tables and placing specific conditions for the retrieval of data. It is another tabular view of the data showing information from multiple tables, resulting in the presentation of the information required, raised in the query.

![]() Q.20. Explain ‘Flexibility’ and ‘Cost of the installation’ as considerations before opting for specific accounting software.

Q.20. Explain ‘Flexibility’ and ‘Cost of the installation’ as considerations before opting for specific accounting software.

Answer: Flexibility: (It may include the following points)

• Related to data entry, availability, and design of various reports.

• Between users (Accountants)

• Between systems.

Cost of installation and maintenance: (It may include the following points in explanation)

• Ability to afford hardware and software

• Cost-benefit analysis and study of available options

• Training of staff, cost of updating

![]() Q.21. Explain any four sub-groups of the Account Group ‘Profit and Loss’

Q.21. Explain any four sub-groups of the Account Group ‘Profit and Loss’

Answer: Any four of the following:

• Sales Account

• Purchase Account

• Direct Income

• Indirect Income

• Direct Expenses

• Indirect Expenses (With appropriate explanation)

![]() Q.22. Explain the steps involved in the installation of computerized accounting software.

Q.22. Explain the steps involved in the installation of computerized accounting software.

Answer: Steps in the installation of CPS:

1. Insert CD in the system

2. Select C: E:, or D: drive from my computer

OR

Start > run > type the filename E:\install.exe

3. The default directories of application, data, and configuration will open in a window. Change the setting if you wish by providing desired file name and drive name.

4. Click on install. The installation process will start and a message of successful installation will appear after its completion. The CD can be removed as the application is successfully installed.

![]() Q.23. What is meant by ‘Conditional formatting’? Explain its benefits.

Q.23. What is meant by ‘Conditional formatting’? Explain its benefits.

Answer: Conditional formatting means a format change, such as background cell shading or font color i.e. applied to a cell when a specified condition for the data in the cell is true. Conditional formatting is often applied to worksheets to find:

1. Data that is above or below a certain value.

2. Duplicate data values.

3. Cells containing specific text.

4. Data that is above or below average

5. Data that falls in the top ten or bottom ten values

Benefits of using conditional formatting:

1. Helps in answering questions that are important for making decisions.

2. Guides with help of using visuals.

3. Helps in understanding the distribution and variation of critical data.